Next: Generating Random Variables From

Up: Generating Random Variables

Previous: Sampling From a Distribution

Index

Click for printer friendely version of this HowTo

There are two primary methods for generating normally distributed

random variables. The first method relies on the central limit theorem

which states that if E and Var

and Var

, then for

independent and identically distributed samples from any distribution

, then for

independent and identically distributed samples from any distribution

has an approximate

has an approximate

distribution, where

distribution, where  is the sample size. The utility in this first method is that it

is very easy to remember off the top of your head and is relatively

easy to compute with a computer.

is the sample size. The utility in this first method is that it

is very easy to remember off the top of your head and is relatively

easy to compute with a computer.

The second method uses a direct transformation, and, while being just

as easy to compute using a computer, is a little tricky to

remember. This method is called the Box-Muller algorithm. The steps

involved are:

- Generate to independent uniform(0,1) variables,

,

,  .

.

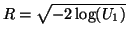

- Let

and

and

- Let

and

and

.

.

where  and

and  are independent normal(0,1) random variables. See

Appendix A.2 for an Octave program that implements

this algorithm.

are independent normal(0,1) random variables. See

Appendix A.2 for an Octave program that implements

this algorithm.

Next: Generating Random Variables From

Up: Generating Random Variables

Previous: Sampling From a Distribution

Index

Click for printer friendely version of this HowTo

Frank Starmer

2004-05-19